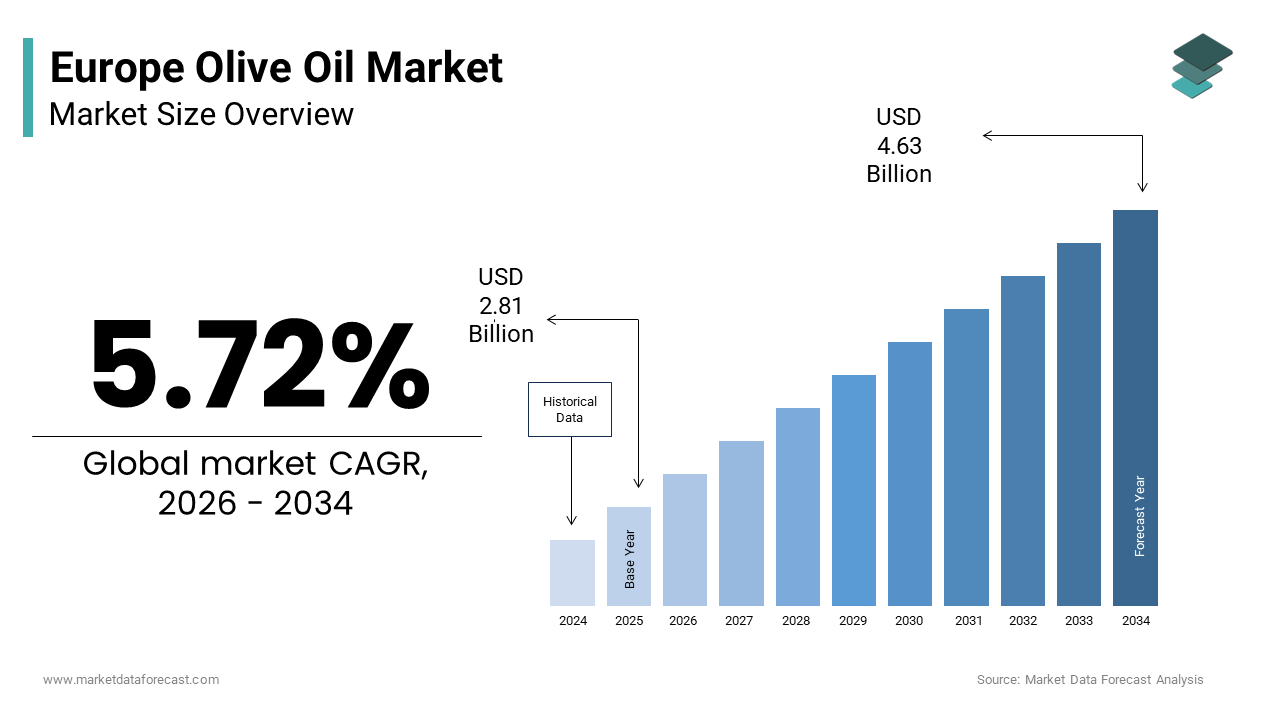

Europe Olive Oil Market Size

The size of the Europe olive oil market was calculated to be USD 2.81 billion in 2025 and is anticipated to be worth USD 4.63 billion by 2034, from USD 2.97 billion in 2026, growing at a CAGR of 5.72% during the forecast period.

Olive oil encompasses the cultivation, extraction, and distribution of oil derived from the fruit of the Olea europaea tree, a commodity deeply embedded in the cultural and culinary fabric of the continent. This sector extends beyond mere gastronomy to represent a critical pillar of the Mediterranean diet, which is recognized globally for its health benefits. The European landscape is uniquely defined by its status as both the largest producer and consumer of olive oil worldwide, with the southern rim of the continent hosting vast groves that define the agrarian identity of nations like Spain, Italy, and Greece. As per Eurostat, the agricultural area dedicated to olive groves in the European Union is extensive, which is illustrating the immense scale of this perennial crop. Furthermore, according to the European Food Safety Authority, health claims have been authorized regarding the protective effects of olive oil polyphenols against oxidative stress, lending scientific weight to consumer preferences. The region also faces distinct climatic vulnerabilities, as the olive tree is highly sensitive to temperature fluctuations and water scarcity, making the market a barometer for broader environmental changes. This convergence of cultural heritage, regulatory endorsement of health benefits, and climatic sensitivity creates a complex ecosystem where tradition meets modern sustainability challenges, which is driving the evolution of production practices and consumption patterns across the continent.

MARKET DRIVERS Escalating Consumer Awareness of Cardiovascular Health Benefits

The profound shift in consumer behavior driven by increasing awareness of the link between olive oil consumption and cardiovascular health is one of the key factors propelling the growth of the European olive oil market. European populations are becoming increasingly health-literate, actively seeking dietary fats that offer protective benefits rather than merely providing calories. As per the European Society of Cardiology, cardiovascular diseases remain the leading cause of death in Europe, which has spurred public health campaigns promoting the Mediterranean diet as a preventive measure. This medical consensus has transformed olive oil from a cooking ingredient into a functional food essential for longevity. Consumers are specifically looking for extra virgin varieties rich in polyphenols and monounsaturated fats, which have been clinically proven to reduce bad cholesterol levels and improve blood vessel function. The demographic trend of an aging population further amplifies this demand, as older individuals prioritize diets that support heart health and cognitive function. Retailers and food service providers have responded by prominently labeling health benefits and sourcing high-quality oils to meet this discerning demand. The integration of olive oil into national dietary guidelines across several European nations reinforces its status as a staple, ensuring sustained growth in consumption volumes as individuals proactively modify their diets to mitigate health risks associated with modern lifestyles.

Deep-Rooted Cultural Significance and Culinary Tradition

The entrenched cultural identity associated with olive oil that serves as a cornerstone of daily life and social rituals across Southern Europe and increasingly influences Northern European palates is further boosting the expansion of the European olive oil market. In countries like Spain, Italy, and Greece, olive oil is not merely a commodity but a symbol of heritage, family, and regional pride, ensuring consistent domestic consumption regardless of price fluctuations. As per UNESCO, the Mediterranean diet, with olive oil as its central element, is recognized as an Intangible Cultural Heritage of Humanity, a designation that reinforces its value and promotes its preservation among younger generations. This cultural reverence translates into high per capita consumption, with households in producing nations often purchasing directly from local mills or cooperatives to maintain authenticity. Furthermore, the globalization of Mediterranean cuisine has exported this cultural appreciation to Northern and Eastern Europe, where consumers associate olive oil with sophistication and gourmet dining. The rise of food tourism and culinary media has further democratized knowledge about olive oil grades and origins, encouraging consumers outside traditional regions to incorporate it into their daily cooking. This cultural diffusion ensures that demand remains robust and expands geographically, as the emotional and social connection to the product drives loyalty and willingness to pay a premium for authentic, region-specific varieties that embody the essence of European culinary tradition.

MARKET RESTRAINTS Severe Impact of Climate Change and Extreme Weather Events

The escalating frequency of extreme weather events linked to climate change that directly threatens olive yields and disrupts supply chains across the continent is impeding the European olive oil market expansion. The olive tree, while resilient, is highly susceptible to prolonged droughts, unseasonal frosts, and heatwaves, all of which have become more prevalent in the Mediterranean basin. As per the European Environment Agency, Southern Europe is warming faster than the global average, with recent years recording historic temperature highs that have caused significant flower abortion and reduced fruit set in major producing regions. Severe droughts in Spain and heatwaves in Italy have led to harvest reductions in certain years, creating volatile supply conditions. These climatic shocks not only diminish the volume of available oil but also compromise quality, as stressed trees produce fruit with different chemical profiles. The unpredictability of weather patterns makes long-term planning difficult for farmers, who face increased costs for irrigation and risk management. Furthermore, the shifting climate zones may eventually render traditional growing areas unsuitable, forcing a geographic relocation of orchards that could take decades to mature. This environmental vulnerability acts as a persistent brake on market growth, introducing uncertainty that affects pricing, availability, and the economic viability of smallholder farmers who form the backbone of the European olive oil sector.

Proliferation of Pests and Diseases Exacerbated by Warming Temperatures

The rising prevalence of pests and plant diseases that are thriving due to warmer winters and changing ecological conditions that favor their reproduction and spread is further hampering the growth of the European olive oil market. The most notorious example is the Xylella fastidiosa bacterium, which has devastated millions of olive trees in parts of Italy and poses a continuous threat to other producing nations. As per the European Commission’s Joint Research Centre, the spread of such pathogens is accelerated by milder winters that fail to kill off pest populations, leading to more aggressive infestations of the olive fruit fly and various fungal infections. These biological threats can wipe out entire orchards, forcing the removal of infected trees and resulting in long-term production losses that take years to recover from as new trees must be planted and matured. The cost of implementing containment measures, such as extensive monitoring, pruning, and biological controls, places a heavy financial burden on producers, particularly small-scale farmers with limited resources. Additionally, strict regulations on pesticide use in the European Union limit the tools available to combat these outbreaks, creating a dilemma between maintaining organic standards and saving crops. The constant battle against evolving biological adversaries undermines yield stability and increases production costs, which is acting as a significant restraint on the market’s ability to meet growing demand consistently.

MARKET OPPORTUNITIES Expansion of Premium and Organic Olive Oil Segments

The rapid growth of the premium and organic olive oil sectors is a promising opportunity in the European olive oil market. As environmental consciousness rises, European shoppers are seeking assurances that their food is produced without synthetic pesticides or fertilizers, aligning with broader wellness and eco-friendly lifestyles. As per the Research Institute of Organic Agriculture, the market for organic food in Europe has been expanding, with olive oil being one of the top categories for conversion to organic farming methods. Producers who obtain certifications such as Protected Designation of Origin or organic labels can command significant price premiums, improving profit margins despite lower yields. This trend encourages farmers to adopt regenerative agricultural practices that enhance soil health and biodiversity, thereby future-proofing their operations against climate risks. Furthermore, the rise of direct-to-consumer sales channels allows small producers to tell their story and highlight the unique terroir of their oil, fostering a deeper connection with buyers. By focusing on quality over quantity, the industry can cater to a niche but lucrative demographic that values transparency and sustainability, opening new revenue streams that offset the challenges of mass production and commoditization.

Innovation in Extraction Technologies and Byproduct Utilization

The adoption of advanced extraction technologies and the valorisation of olive mill byproducts present a substantial opportunity for the European olive oil market. Modern continuous centrifugation systems and cold extraction techniques allow producers to maximize oil yield while preserving delicate aromatic compounds and nutritional properties, appealing to quality-conscious consumers. As per the International Olive Council, innovations in processing can reduce water usage and energy consumption, addressing sustainability concerns and lowering operational costs. Moreover, the industry is increasingly exploring the potential of olive pomace and wastewater, traditionally considered waste, to produce biofuels, natural antioxidants, and cosmetic ingredients. This shift transforms waste streams into valuable revenue sources, improving the overall economics of olive oil production. Companies investing in biorefineries can extract high-value polyphenols for pharmaceutical and nutraceutical applications, diversifying their income beyond culinary oil. The integration of digital tools for precision agriculture, such as sensors for soil moisture and drone monitoring for tree health, further optimizes resource use and predicts harvest outcomes. By embracing technological advancement and circular principles, the European olive oil sector can enhance its resilience, reduce its environmental footprint, and unlock new value chains that drive sustainable growth.

MARKET CHALLENGES Intensifying Global Competition and Adulteration Issues

The fierce competition from non-European producers and the persistent issue of fraud and adulteration that erodes consumer trust and destabilizes prices is challenging the expansion of the European olive oil market. Countries like Tunisia, Turkey, and Morocco have significantly increased their production capacities and export volumes, often offering lower-priced alternatives that compete directly with European oils in key markets. As per consumer protection agencies in Europe, olive oil sold as extra virgin is sometimes blended with lower quality seed oils or inferior grade olive oils, a practice that undermines the reputation of authentic European producers. This fraud not only deceives consumers but also depresses market prices, making it difficult for legitimate high-cost European farmers to compete. The complexity of the global supply chain makes tracking origin and verifying purity challenging, despite efforts to implement stricter labeling laws and blockchain tracing technologies. The fear of purchasing counterfeit products leads to hesitation among buyers, potentially stifling demand for premium categories. Combating this illicit trade requires coordinated international enforcement and substantial investment in authentication technologies, yet the sheer scale of the problem remains a daunting obstacle that threatens the integrity and economic viability of the genuine European olive oil industry.

Structural Fragmentation and Aging Farmer Demographics

The fragmentation of land ownership and the advancing age of the farmer population are further challenging the expansion of the olive oil market in Europe. A vast majority of European olive groves are managed by smallholder farmers operating on plots of less than five hectares, often as a secondary source of income or a hobby, limiting their ability to invest in modern machinery or efficient irrigation systems. As per the European Commission, the average age of farmers in the European Union is high, with a significant portion of olive growers being even older, raising concerns about succession and the future viability of these orchards. Younger generations are often reluctant to take over labour-intensive farming activities with uncertain returns, leading to the abandonment of marginal groves and a reduction in cultivated area. This demographic shift results in a lack of innovation and professionalization, as small, aging farmers struggle to adopt new technologies or meet stringent certification requirements. The fragmented nature of the sector also weakens bargaining power against large distributors and processors, squeezing profit margins further. Without significant consolidation, cooperative strengthening, or policy interventions to attract young talent, the structural weaknesses of the European olive oil sector threaten its long-term competitiveness and capacity to sustain production levels.

REPORT COVERAGE

REPORT METRIC

DETAILS

Market Size Available

2025 to 2034

Base Year

2025

Forecast Period

2026 to 2034

CAGR

5.72%

Segments Covered

By Type, Distribution Channel, And Region

Various Analyses Covered

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities

Regions Covered

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic

Market Leaders Profiled

Del Monte Food, Inc., Cargill, Inc., Deoleo, Ybarra, Gruppo Salov, Sovena Group, Jaencoop, Macario SA, Maeva Group, and Lamasia

SEGMENTAL ANALYSIS By Type Insights

The extra virgin olive oil segment dominated the market by commanding for 54.4% of the reginal market share in 2025. The dominance of extra virgin olive oil segment in the European market is primarily driven by its superior sensory profile, highest nutritional value, and strict regulatory definitions that guarantee quality to consumers. Unlike lower grades, Extra Virgin Olive Oil must be obtained solely by mechanical means without heat or chemicals, ensuring the preservation of natural antioxidants and polyphenols. As per the European Commission, this oil must meet strict standards for acidity and sensory quality, a benchmark that has become central to quality assurance among European shoppers. This strict definition fosters deep consumer trust, as buyers increasingly view the “Extra Virgin” label as a guarantee of purity and health benefits amidst concerns over adulteration in the broader edible oil market. The mandatory labeling laws in Europe require clear distinction between grades, empowering consumers to make informed choices that favor the highest quality option. Furthermore, the presence of Protected Designation of Origin labels on many Extra Virgin varieties reinforces the perception of authenticity and regional superiority. This regulatory endorsement combined with heightened consumer vigilance ensures that Extra Virgin Olive Oil remains the preferred choice for health-conscious individuals and culinary enthusiasts who prioritize ingredient integrity.

The processed olive oil segment is anticipated to record a CAGR of 7.4% over the forecast period in the European market due to its cost-effectiveness, high smoke point suitability for industrial food processing, and increasing adoption in the food service sector. Restaurants, cafeterias, and fast-food chains across Europe operate on thin margins and require large volumes of oil for frying and sautéing, where the subtle flavor nuances of Extra Virgin Olive Oil are often lost during high-heat cooking. As per the European Hospitality Association, the recovery of the hospitality sector has led to rising demand for bulk cooking oils that offer stability and economic viability. Processed olive oil, which is refined to remove impurities and neutralize strong flavors, provides a high smoke point ideal for deep frying without breaking down, while costing significantly less than its Extra Virgin counterpart. This price advantage allows food service operators to offer “olive oil cooked” dishes at competitive prices, appealing to budget-conscious diners. Furthermore, the consistency of refined oil ensures uniform taste across franchise locations, a key requirement for chain restaurants. As the food service sector continues to expand and seek efficiency, the volume demand for processed olive oil is set to grow rapidly, driving the segment’s accelerated growth trajectory.

By Distribution Channel Insights

The groceries segment held 66.5% of the regional market share in 2025. The dominance of groceries segment in the European market can be credited to its ubiquitous presence, extensive product variety, and the habitual nature of weekly food shopping. These large-format retailers offer the convenience of one-stop shopping, allowing consumers to purchase olive oil alongside all other daily necessities in a single trip. As per Eurostat retail data, food and beverage expenditure in European households is concentrated in large grocery stores, which is reflecting a shopping culture centred around weekly bulk buying. The sheer scale of these outlets enables them to stock a comprehensive range of olive oil brands, from mass-market private labels to premium imported varieties, catering to diverse consumer preferences and budget levels. The strategic placement of olive oil in prominent aisles, often accompanied by promotional displays and tasting stations, maximizes visibility and encourages impulse purchases. Furthermore, the reliability of stock availability and the competitive pricing driven by the bargaining power of large retail chains make groceries the preferred channel for price-sensitive shoppers. The integration of loyalty programs and digital coupons within these chains further incentivizes repeat purchases, cementing the position of supermarkets and hypermarkets as the primary conduit for olive oil distribution.

The online stores segment is a promising segment and is estimated to witness the fastest CAGR of 15.5% over the forecast period owing to the rapid digitization of grocery shopping, the rise of direct-to-consumer models from artisanal producers, and the demand for specialized and premium products. As per the European E-Commerce Report, online grocery shopping has been expanding, accelerated by the pandemic and sustained by the convenience of home delivery and click-and-collect services. Consumers increasingly value the ability to browse extensive catalogs, read detailed product descriptions, and compare prices from the comfort of their homes, avoiding the crowds and time constraints of physical stores. For heavy items like large tins or multi-packs of olive oil, the home delivery option eliminates the physical burden of carrying groceries, appealing particularly to elderly individuals and busy professionals. Retailers have optimized their digital interfaces to highlight fresh and premium categories, ensuring that olive oil is easily discoverable and accessible. The integration of AI-driven recommendations and personalized offers based on past purchase history further enhances the online shopping journey, encouraging larger basket sizes and frequent reordering. As logistics networks become more efficient and delivery windows more flexible, the barrier to buying perishable and bulk goods online diminishes, unlocking a vast potential for growth in the digital channel.

REGIONAL ANALYSIS Spain Olive Oil Market Analysis

Spain dominated the olive oil market in Europe in 2025 with 39.1% of the regional market share. The dominance of Spain is majorly due to its vast cultivation area, dominant production volume, and deep cultural integration of olive oil into daily life. The Spanish market is characterized by its role as the world’s largest producer and exporter, with Andalusia alone accounting for a significant portion of global output. As per the Spanish Ministry of Agriculture, Fisheries and Food, the country possesses extensive olive groves yielding large volumes of oil annually, which supply both domestic needs and international markets. The domestic consumption pattern is robust, with Spaniards exhibiting one of the highest per capita consumption rates globally, viewing olive oil as an essential staple rather than a luxury. The presence of powerful cooperatives and large industrial bottlers ensures efficient processing and distribution, maintaining Spain’s competitive edge in pricing and volume. Furthermore, the government’s active promotion of Protected Designation of Origin labels supports the premiumization of Spanish oils, enhancing their reputation abroad. The combination of agrarian scale, industrial capacity, and cultural ubiquity cements Spain’s position as the primary engine of the European olive oil sector, influencing global prices and supply dynamics.

Italy Olive Oil Market Analysis

Italy had a promising share of the European olive oil market in 2025. The growth of Italy in the European market is attributed to its renowned reputation for quality, strong branding, and a sophisticated domestic consumer base that prioritizes premium and regional varieties. The Italian market is distinguished by its focus on high-value Extra Virgin Olive Oil, with a multitude of Protected Designation of Origin and Protected Geographical Indication labels that certify authenticity and terroir. As per the Italian National Institute of Statistics, despite producing less volume than Spain, Italy often commands higher price points due to its association with gourmet cuisine and superior sensory profiles. The domestic market is highly discerning, with consumers willing to pay a premium for locally sourced, cold-pressed oils from regions like Tuscany, Puglia, and Liguria. Italy also serves as a major hub for blending and packaging, importing bulk oil from other Mediterranean countries to refine and bottle under prestigious Italian brands for re-export. This value-added activity strengthens its market position significantly. The strong influence of Italian culinary culture globally further boosts demand for Italian-labeled oils, creating a virtuous cycle of brand equity and export success. The synergy between quality perception, branding excellence, and culinary heritage drives Italy’s significant contribution to the regional market.

Greece Olive Oil Market Analysis

Greece is anticipated to account for a prominent share of the European olive oil market over the forecast period owing to its exceptionally high per capita consumption, the predominance of small-scale family farming, and a strong orientation toward organic production. The Greek market is unique in that a large proportion of its output is classified as Extra Virgin Olive Oil, reflecting traditional harvesting and milling practices that prioritize quality over quantity. As per the Hellenic Ministry of Rural Development and Food, Greece has the highest per capita consumption of olive oil globally, indicating a profound cultural dependency on the product. The landscape is dominated by smallholder farmers who often adhere to traditional methods, resulting in oils with distinct character and high polyphenol content. There is a growing shift toward organic certification, with Greece holding a leading position in Europe for organic olive oil acreage. This focus on sustainability and quality appeals to niche international markets seeking premium products. The domestic market remains stable and resilient, supported by strong local traditions and the integral role of olive oil in the Greek diet. The combination of ultra-high-quality standards, organic leadership, and intense domestic usage ensures Greece remains a pivotal player in the European olive oil landscape.

France Olive Oil Market Analysis

France is expected to exhibit a healthy CAGR in the European olive oil market during the forecast period. The focus of France on niche premium production, strong regional identities, and a growing domestic demand for high-quality local oils are propelling the French market expansion. The French market is smaller in volume compared to its southern neighbours but excels in the ultra-premium segment, with regions like Provence and Corsica producing highly sought-after oils with specific flavor profiles. As per the French National Interprofessional Office for Fruits, Vegetables, Wines and Horticulture, French consumers are increasingly conscious of origin and quality, favoring locally produced oils with Protected Designation of Origin status. The domestic production is limited by geography but commands very high prices, catering to a discerning clientele that views olive oil as a gastronomic product. France is also a major importer and re-exporter, blending imported oils to meet the demands of its large food service and retail sectors. The government’s support for agricultural diversification and sustainable practices encourages the maintenance of olive groves as part of the cultural landscape. The rise of agritourism and direct sales from mills to consumers further strengthens the local market. The blend of exclusivity, regional pride, and gourmet positioning allows France to occupy a lucrative and influential niche in the European market.

Germany Olive Oil Market Analysis

Germany is estimated to hold a notable share of the European olive oil market during the forecast period owing to its status as a major non-producing importer, a health-conscious consumer base, and a robust retail infrastructure that drives volume sales. Unlike the Mediterranean nations, Germany does not produce olive oil commercially, yet it stands as one of the largest consumption markets in Northern Europe. As per the German Federal Office for Agriculture and Food, olive oil consumption in Germany has been rising steadily, driven by the widespread adoption of the Mediterranean diet for health reasons. German consumers are highly educated about nutrition and actively seek out Extra Virgin Olive Oil for its cardiovascular benefits, often prioritizing organic and fair-trade certifications. The market is dominated by large supermarket chains that offer a wide range of options from various producing countries, fostering intense competition and keeping prices accessible. The strong demand for private label products and the popularity of bulk purchasing formats contribute to high volume turnover. The absence of domestic production means the market is entirely dependent on imports, making Germany a critical destination for surplus oil from Spain, Italy, and Greece. This import-driven demand, fueled by health awareness and retail efficiency, secures Germany’s place as a vital component of the European olive oil consumption landscape.

COMPETITION OVERVIEW

The competition in the Europe olive oil market is intensely fragmented and characterized by a fierce rivalry between large multinational corporations, powerful cooperatives, and numerous small-scale artisanal producers vying for shelf space and consumer loyalty. Global giants leverage their extensive distribution networks and massive marketing budgets to dominate supermarket aisles with well-known branded products. However, local cooperatives and family-owned mills are gaining traction by emphasizing authenticity, regional heritage, and superior quality that resonate with discerning consumers seeking traceability. Competitive pressure is heightened by the prevalence of private label brands offered by major retailers, which compete directly on price and often undercut established names. The market faces additional complexity due to fluctuating production volumes caused by climate change and pest outbreaks, leading to volatile pricing dynamics that challenge profitability for all participants. Fraud and adulteration issues further erode consumer trust, forcing legitimate producers to invest heavily in certification and transparency technologies. The battle for differentiation now centers on sustainability credentials, organic status, and unique flavor profiles rather than just price. This dynamic environment demands constant adaptation and strategic agility to sustain growth and capture opportunities in the evolving European olive oil sector.

KEY MARKET PLAYERS

A few major players of the Europe olive oil market include

Del Monte Food, Inc Cargill, Inc Deoleo Ybarra Gruppo Salov Sovena Group Jaencoop Macario SA Maeva Group Lamasia Top Strategies Used by Key Market Participants

Key players in the Europe olive oil market primarily employ vertical integration strategies to control the entire supply chain from orchard to bottle, ensuring quality consistency and mitigating supply risks. Companies are increasingly investing in sustainable farming practices and organic certification to appeal to environmentally conscious consumers and comply with strict regulatory standards. Strategic acquisitions of smaller regional producers allow large corporations to expand their portfolio of premium brands and secure access to high-quality raw materials. Major participants focus heavily on brand differentiation through storytelling and protected designation of origin labels to justify premium pricing in a crowded marketplace. Expansion into emerging markets and diversification of product formats such as flavored oils and spray versions serve as vital tactics to capture new demographic segments. Furthermore, firms are leveraging digital platforms and direct-to-consumer models to build stronger customer relationships and gather valuable data on purchasing behaviors. These multifaceted strategies enable market leaders to maintain competitiveness and drive growth in a volatile and highly fragmented industry landscape.

Leading Players in the Europe Olive Oil Market Deoleo S.A. stands as a global leader in the olive oil sector with deep roots in Spain and a vast international footprint that spans multiple continents. The company contributes significantly to the global market by managing an extensive portfolio of renowned brands that cater to diverse consumer preferences across retail and food service channels. Recently Deoleo has focused on optimizing its supply chain efficiency and expanding its sourcing network to ensure consistent quality despite climatic volatility. The firm actively invests in sustainability initiatives to support olive growers and reduce environmental impact throughout its value chain. By leveraging advanced blending technologies and rigorous quality control systems, Deoleo maintains high standards for its extra virgin and premium offerings. Their strategic emphasis on brand innovation and digital marketing helps connect with younger consumers seeking healthy and authentic products. These efforts reinforce its position as a dominant force capable of navigating market fluctuations while delivering value to customers worldwide through reliable and high-quality olive oil solutions. Sovena Group operates as a major multinational player with a strong presence in Europe and a significant contribution to the global olive oil trade through its diverse brand portfolio and vertical integration. The company controls every step of the production process from orchard management to bottling and distribution, ensuring traceability and quality assurance. Recent actions include expanding its organic olive oil ranges and investing in modern extraction facilities to enhance efficiency and product purity. Sovena actively promotes sustainable farming practices among its network of suppliers to mitigate climate risks and support rural communities. The group also focuses on developing innovative packaging solutions that extend shelf life and reduce plastic waste. By strengthening its logistics network and forging strategic partnerships with retailers globally, Sovena ensures wide availability of its products. Their commitment to research and development allows them to introduce new flavor profiles and functional oils that meet evolving consumer demands. This holistic approach solidifies its reputation as a key innovator and reliable supplier in the international olive oil landscape. Borges Agricultural and Industrial Nuts S.A. is a prominent family-owned enterprise based in Spain that plays a pivotal role in the European and global olive oil markets through its premium brands and diversified product offerings. The company is known for its dedication to quality and innovation, often pioneering new formats such as single-dose servings and flavored oils. Recently Borges has strengthened its market position by acquiring strategic assets to expand its production capacity and secure raw material supplies. The firm places a strong emphasis on sustainability and social responsibility, implementing programs to support biodiversity and water conservation in olive growing regions. Borges also invests heavily in marketing campaigns that highlight the health benefits and culinary versatility of its oils. By expanding its distribution channels into emerging markets and enhancing its e-commerce capabilities, the company reaches a broader audience. Their focus on premiumization and brand differentiation allows them to command higher price points and build loyal customer bases. This strategic vision ensures their continued growth and influence in the competitive global olive oil industry. MARKET SEGMENTATION

This research report on the Europe olive oil market has been segmented and sub-segmented based on type, distribution channel & region.

By Type

Virgin Olive Oil Extra Virgin Olive Oil Processed Olive oil

By Distribution Channel

By Region

UK France Spain Germany Italy Russia Sweden Denmark Switzerland Netherlands Turkey Czech Republic Rest of Europe

Dining and Cooking